Across the globe, 1.5 billion people remain unbanked, without access to even the most basic financial services. For the rest, fewer than 50% of the banked population qualify for formal credit, limiting both financial inclusion and lending growth. In an era where traditional credit models struggle to assess evolving financial behaviors, AI credit scoring is emerging as a strategic differentiator for banks and fintechs alike.

But how can financial institutions unlock the credit potential of millions who remain “invisible” to legacy scoring systems?

How can AI enable lenders to balance inclusion with risk assurance?

And what does the future of credit decisioning look like when driven by real-time behavioral data rather than historical repayment patterns?

AI-driven credit scoring leverages advanced machine learning models to assess both ability and willingness to repay, drawing from a far broader and more dynamic set of inputs than traditional methods. Beyond standard metrics like income and credit history, modern AI systems incorporate…

This multidimensional approach transforms credit evaluation from a backward-looking exercise into a predictive and adaptive intelligence model. The result? Higher accuracy in risk assessment, faster loan approvals, and greater financial accessibility for individuals and small businesses previously excluded from the system.

Recent studies suggest that AI-based credit models can improve default prediction accuracy by up to 30% while expanding credit access to over 20% more applicants without increasing portfolio risk. For financial leaders, the implications are profound, like rethinking risk, redefining reach, and reengineering trust in the digital economy.

To explore how machine learning is revolutionizing the fundamentals of credit decisioning and what it means for your institution’s lending strategy, read our deep dive into Credit Scoring Powered by AI and Machine Learning.

At its core, credit scoring is the quantitative measure of trust, like an assessment of an individual’s or business’s ability and willingness to repay borrowed funds. It sits at the very foundation of modern financial systems, influencing decisions that range from personal loans and mortgages to corporate credit lines and trade financing.

Traditionally, credit scores have been derived from a narrow band of historical data, like past borrowing patterns, repayment history, and outstanding liabilities. While these parameters have long served as the industry standard, they often fail to capture the nuanced realities of modern consumers, especially those operating in cash-driven, informal, or gig-based economies.

For financial institutions, the implications are far-reaching. A static, legacy scoring model can undermine both growth and inclusion, excluding potentially creditworthy individuals while exposing lenders to unquantified risks. On the other hand, a more intelligent and adaptive approach, powered by AI and data analytics, can expand access, enhance accuracy, and fuel more sustainable lending portfolios.

In essence, credit scoring is like an economic enabler. It determines who participates in the formal economy, how capital is allocated, and how institutions manage risk at scale. As global economies digitalize and new forms of financial behavior emerge, the ability to measure creditworthiness dynamically and fairly is becoming a key competitive differentiator.

The question for today’s financial leaders is no longer “Should we modernize credit scoring?” but rather “How fast can we adapt before the models of yesterday constrain the markets of tomorrow?”

Credit scoring has come a long way from its origins as a manual, intuition-based judgment to today’s data-driven, algorithmic intelligence systems. Its evolution mirrors the transformation of the financial ecosystem itself, from relationship banking to digital decisioning.

In the mid-20th century, creditworthiness was largely determined by human assessors who relied on personal relationships, qualitative judgments, and limited financial records. While this approach provided context, it lacked consistency, scale, and fairness. The introduction of statistical scoring models in the 1980s marked a significant leap by transforming subjective assessments into standardized numerical scores. Credit bureaus emerged as the custodians of financial data, enabling lenders to automate and scale decisions.

However, traditional models came with their own limitations. Built primarily on historical repayment data, they struggled to assess individuals with thin or non-existent credit histories, particularly in emerging markets. As a result, millions remained credit invisible, and financial inclusion plateaued despite advances in data collection.

The digital era has fundamentally changed this equation. With the proliferation of smartphones, digital payments, and open banking frameworks, the volume and variety of alternative data have exploded. Today, modern credit scoring incorporates everything from real-time transaction analytics to behavioral signals and employment stability. This shift marks the transition from static, rule-based systems to dynamic, self-learning AI models capable of adapting to new borrower patterns.

In many ways, AI-driven credit scoring represents the next frontier, blending data science, behavioral analytics, and economic insight to create a more equitable and forward-looking credit ecosystem. It not only improves prediction accuracy but also redefines who gets access to credit and under what terms.

For leaders in banking and fintech, understanding this evolution is about positioning their institutions at the forefront of financial innovation. The future of lending will belong to those who can translate data into trust, and trust into opportunity.

At its essence, AI-based credit scoring algorithms use machine learning models to assess the probability of default or repayment behavior far more dynamically than traditional statistical models.

Unlike conventional scoring systems that rely on fixed weightings and linear relationships, AI models can detect hidden patterns, analyze nonlinear dependencies, and continuously learn from new data.

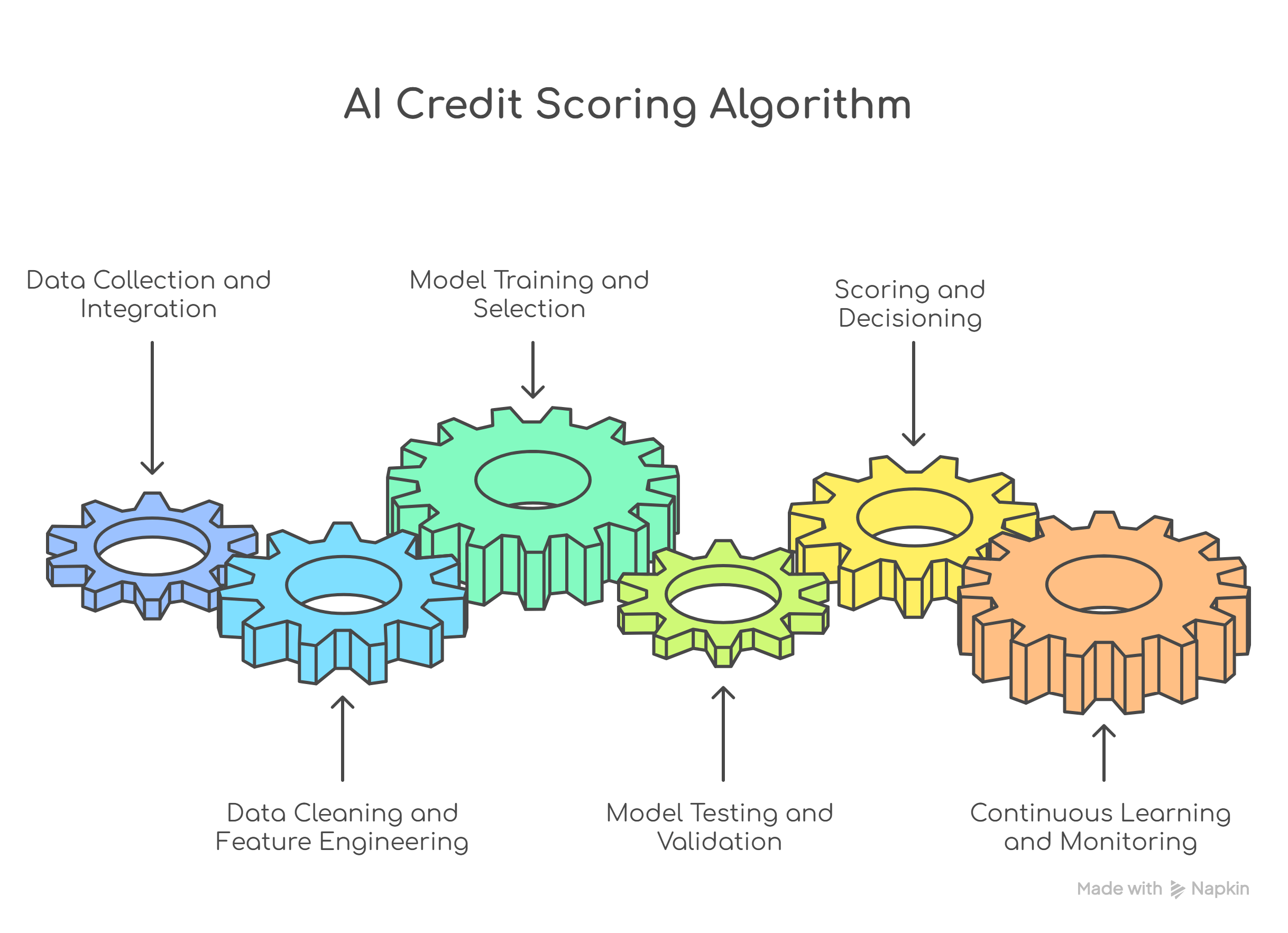

The algorithmic backbone typically follows a structured process designed to transform raw data into actionable insights.

AI models begin by aggregating structured and unstructured data from multiple sources, including bank statements, payment histories, employment data, digital footprints, and even psychometric or behavioral indicators. This phase ensures that the system has a 360° view of the borrower, far beyond what traditional credit bureaus can offer.

Raw data is rarely ready for modeling. Machine learning systems perform extensive preprocessing by removing inconsistencies, handling missing values, and normalizing variables.

Data scientists then engineer features (variables that influence creditworthiness) such as spending-to-income ratios, transaction frequencies, or payment regularities.

Here, the algorithm learns to predict repayment likelihood by analyzing historical borrower outcomes. Common model types include:

The model is then fine-tuned through hyperparameter optimization and cross-validation to achieve maximum accuracy and stability.

Before deployment, the model is tested against separate validation datasets to ensure it performs reliably under real-world conditions. Key metrics such as AUC-ROC, Gini coefficient, and Precision-Recall are used to measure performance and minimize bias.

Once validated, the algorithm generates an AI-driven credit score for each applicant, a probabilistic value representing repayment likelihood. This score can then feed into automated decision engines that determine credit limits, pricing tiers, or approval workflows.

Unlike static models, AI scoring systems continuously learn from new borrower data, market conditions, and repayment trends. Through model retraining and drift detection, institutions maintain accuracy, compliance, and fairness over time.

For decades, credit scoring has relied on a narrow data foundation, like income statements, repayment history, and outstanding loans. While effective for established borrowers, these inputs have excluded millions who operate outside formal credit systems. The challenge for financial institutions has been clear: how do you assess the creditworthiness of those with little or no credit footprint?

This is where AI fundamentally changes the paradigm.

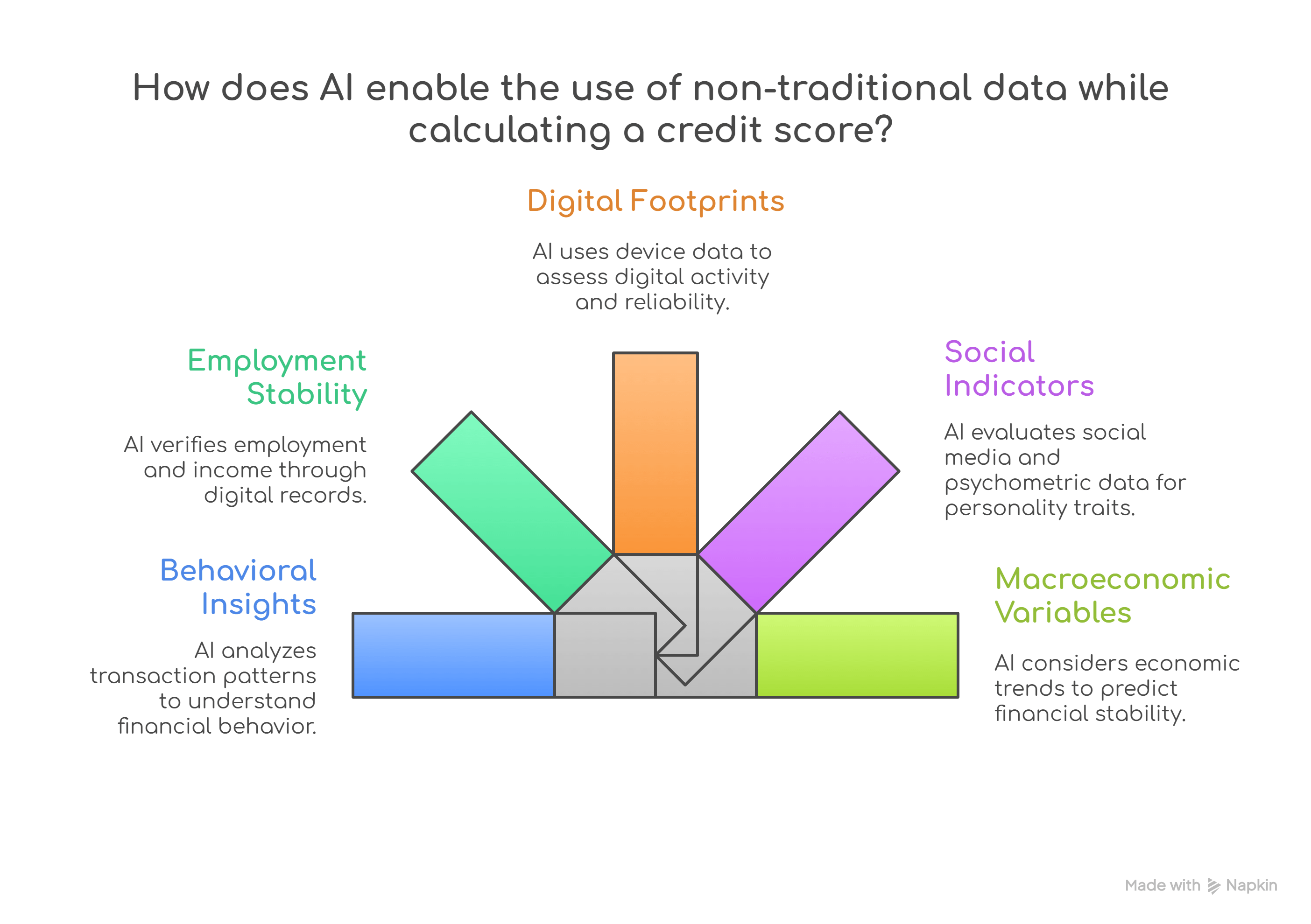

AI-driven credit scoring systems can ingest, interpret, and learn from vast streams of non-traditional or alternative data, the kind that conventional models were never designed to process. These data sources, once considered irrelevant or inaccessible, now offer powerful signals of financial behavior, stability, and intent.

AI models can analyze spending habits, savings frequency, digital payment behavior, and even transaction patterns to infer a borrower’s financial discipline. For example, regular utility bill payments or consistent mobile recharge activity can serve as indicators of reliability, even in the absence of a formal credit history.

Machine learning algorithms assess employment continuity, salary inflows, gig payments, and career trajectories to identify income stability and predict repayment capacity. This is especially relevant for self-employed professionals and gig workers, whose income streams may be irregular yet sustainable.

AI can also interpret subtle digital signals, mobile usage patterns, online purchase behaviors, app engagement, and device metadata to create behavioral profiles. These patterns, when analyzed responsibly and ethically, can highlight attributes like consistency, trustworthiness, and spending prudence.

Advanced models even incorporate psychometric data (responses to structured digital questionnaires) or social network analysis to assess traits such as responsibility and financial intent, like the areas where traditional data provides no visibility.

Beyond the individual, AI integrates geospatial data, regional economic indicators, and market dynamics to contextualize risk, ensuring that a borrower’s score reflects both personal capability and environmental factors.

By blending traditional and non-traditional data, AI allows lenders to move from risk avoidance to risk discovery. It expands the addressable market, enabling institutions to safely lend to thin-file or previously unbanked populations, while maintaining regulatory compliance and credit discipline.

Studies indicate that AI models using alternative data can increase credit access by up to 25-30% without compromising risk performance. For C-suite leaders, the message is clear that the future of lending will be shaped not by how much data you have, but by how intelligently your systems interpret it.

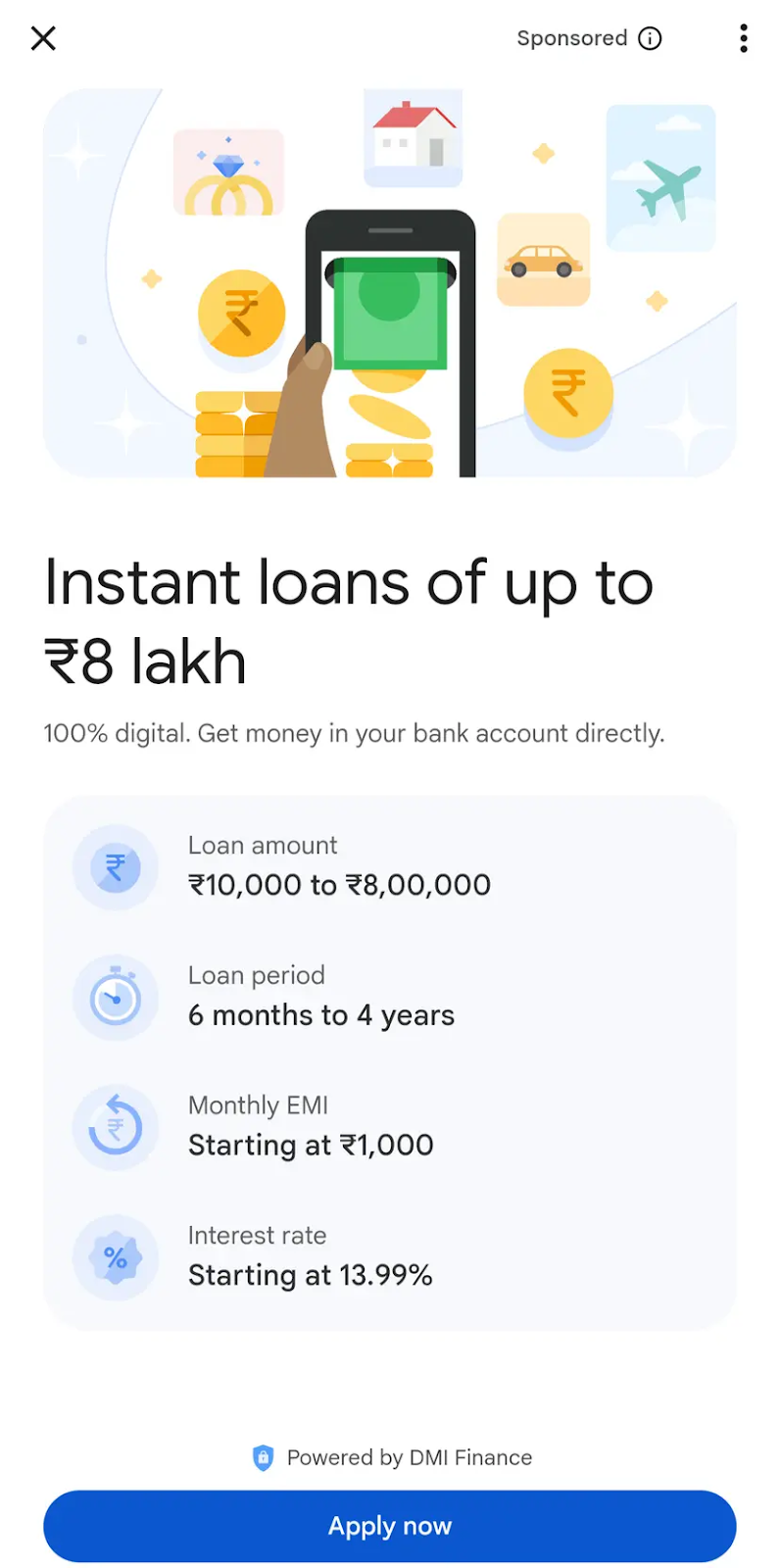

AI-driven credit scoring is already transforming decision-making across some of the world’s most recognized financial and fintech platforms. Leading brands are harnessing the power of machine learning and behavioral analytics to expand credit access, personalize lending, and reduce portfolio risks.

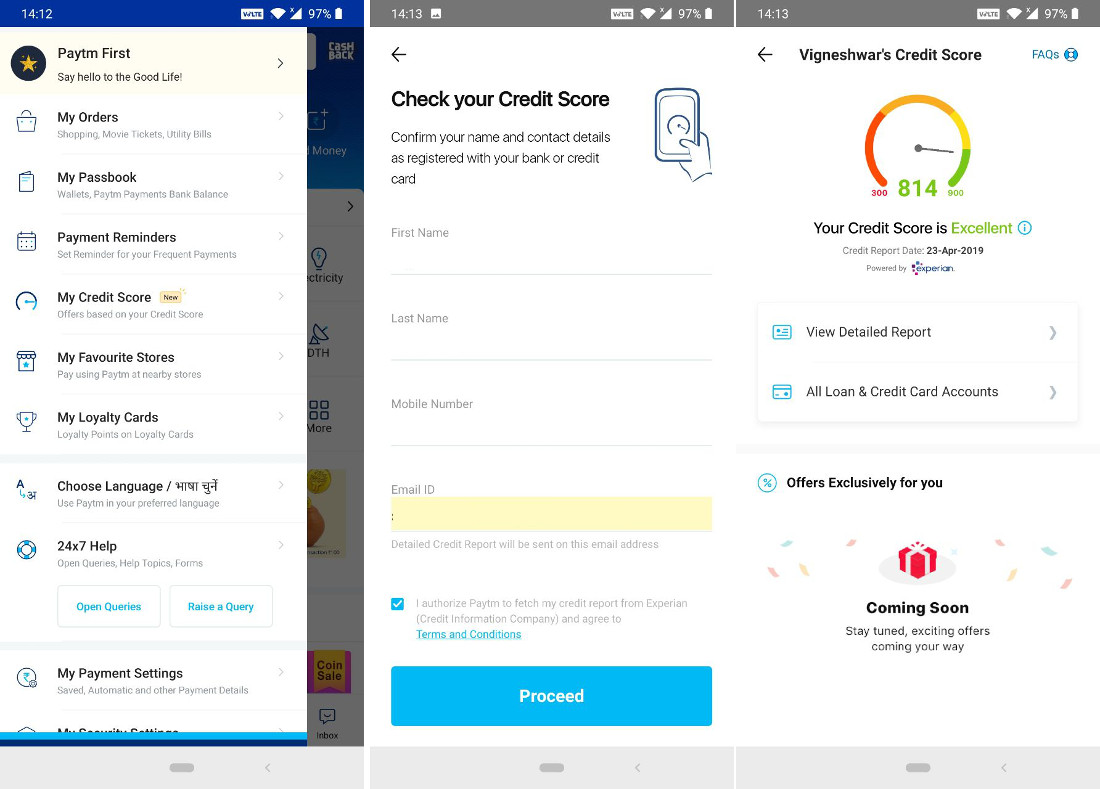

CRED leverages AI algorithms to evaluate users’ repayment behaviors, credit utilization, and transaction histories with extraordinary precision. Beyond traditional bureau data, its scoring models analyze spending patterns, repayment discipline, and digital activity to offer exclusive credit cards and lending options.

Paytm uses AI and data analytics to assess creditworthiness for millions of users, including those without formal credit histories. Its scoring system draws from wallet transactions, bill payments, mobile recharges, and purchase behaviors, allowing Paytm to extend microloans and Buy-Now-Pay-Later (BNPL) services responsibly.

Google Pay’s partnership-driven lending model utilizes AI-powered credit scoring to help partner banks and NBFCs evaluate risk dynamically. By analyzing transaction frequency, payment reliability, and contextual behavior, Google Pay enables lenders to make faster, more informed decisions, especially in instant, small-ticket loans.

These platforms illustrate a broader industry shift, from static, rule-based credit assessments to adaptive, data-rich, and inclusive AI scoring ecosystems. As adoption accelerates, the ability to integrate intelligent credit decisioning at scale will become a key competitive advantage for every fintech and financial institution.

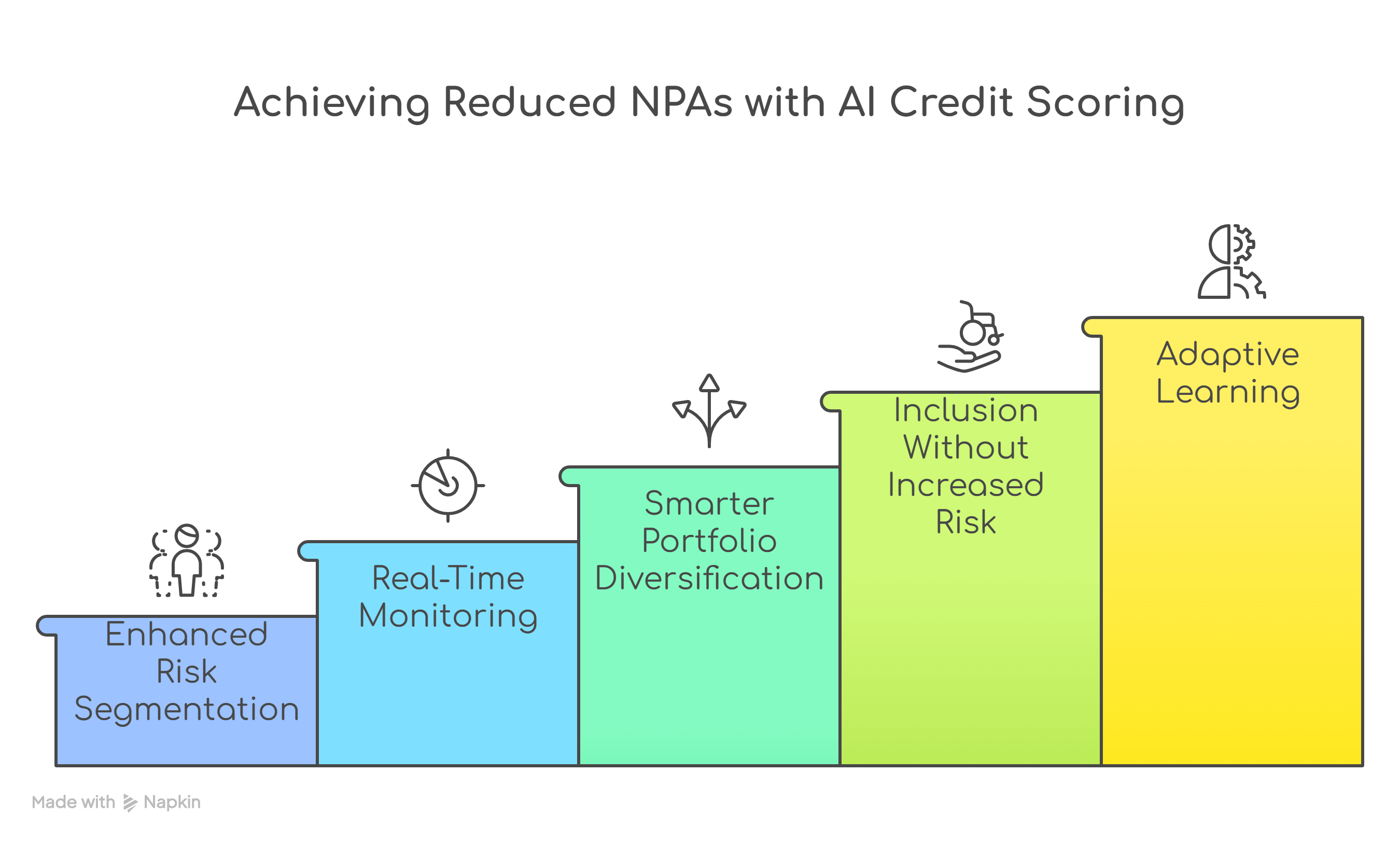

For financial institutions worldwide, Non-Performing Assets (NPAs) represent not just bad loans, but eroded profitability, constrained liquidity, and impaired investor confidence. Traditional credit assessment methods, largely static, manual, and backward-looking, have struggled to accurately identify early signs of risk, especially in volatile markets. The result was delayed interventions, inefficient recovery mechanisms, and mounting non-performing portfolios.

The introduction of AI-powered credit scoring has been a turning point. By infusing predictive intelligence into credit risk management, banks and fintechs have been able to detect, prevent, and mitigate default risks far earlier in the lending cycle.

Conventional scoring models often rely on a limited set of historical variables such as repayment history or debt-to-income ratios. AI systems, by contrast, analyze thousands of data points, including real-time cash flows, spending trends, and even behavioral signals, to build a multidimensional borrower profile.

Machine learning models can predict delinquency risks up to 20-30% more accurately than traditional models, allowing institutions to calibrate lending limits, tailor interest rates, and proactively restructure at-risk portfolios. This predictive precision directly translates into lower credit losses and healthier asset books.

AI models continuously monitor borrower behavior to flag potential signs of distress. For instance, a sudden drop in transaction activity, delayed bill payments, or deviations from income patterns can trigger automated alerts to risk teams.

This early-warning capability enables banks to initiate preventive engagement by offering restructuring options or financial counselling before defaults occur.

According to industry studies, such AI-driven monitoring can reduce NPAs by up to 25-40% in portfolios exposed to retail and SME segments.

AI systems also provide portfolio-level intelligence, helping risk managers identify concentration risks across sectors, geographies, or borrower profiles.

By simulating macroeconomic and borrower-level scenarios, institutions can optimize credit exposure and create dynamic lending strategies that adapt to changing market conditions.

This data-driven approach helps balance growth with prudence, reducing systemic risks that often lead to NPA accumulation.

Historically, financial inclusion came with the perceived trade-off of higher NPAs. AI-based credit scoring challenges this assumption.

By leveraging alternative data, such as digital payments, employment records, and behavioral analytics, lenders can confidently extend credit to thin-file customers while maintaining risk discipline.

The result is responsible inclusion: expanding the customer base without compromising portfolio health.

Unlike traditional credit models that degrade over time, AI systems continuously learn from new data and repayment behaviors. When defaults do occur, models automatically recalibrate to strengthen future risk predictions, ensuring that the credit scoring engine becomes smarter with every cycle.

This self-optimizing mechanism builds institutional resilience, especially in unpredictable or high-growth lending environments.

Therefore, artificial intelligence credit scoring has transformed risk management from a reactive to a proactive, predictive discipline. Financial institutions adopting these models have reported:

Beyond immediate financial gains, the strategic value lies in trust and stability. As AI redefines how lenders measure, monitor, and manage credit risk, it equips financial institutions with the intelligence to lend smarter, not just faster.

The outcome is a new era of data-driven credit governance, where decisions are informed, inclusion is responsible, and asset quality is sustainably preserved.

At Antino, we help financial innovators move beyond conventional credit assessment by embedding AI-driven intelligence directly into their lending ecosystem. Our experts design and implement end-to-end credit scoring frameworks that leverage advanced machine learning, real-time analytics, and alternative data streams by transforming how fintech platforms evaluate, underwrite, and manage credit risk. From data architecture and model development to regulatory-grade security and seamless API integration, we ensure your solution is future-ready, compliant, and built for scale.

In an era where precision, agility, and trust define financial growth, Antino stands as a strategic AI development services partner. We enable fintechs and financial institutions to accelerate inclusion, enhance portfolio quality, and unlock new lending opportunities through intelligent automation and predictive insights. With Antino, you operationalize smarter decision-making that drives measurable business outcomes and sustainable impact across the credit lifecycle. So, contact our FinTech experts right away!

.png)