Sending money today feels effortless. But pause for a second, when was the last time you used cash for a transfer or stood in a queue for a wire transfer?

Exactly.

Digital remittances and peer-to-peer payments are growing at an incredible pace across the globe. What used to take hours or even days, with high fees and multiple intermediaries, now happens in seconds. Cross-border transfers, splitting bills, paying freelancers, everything has shifted to real-time, mobile-first experiences.

And this shift is only getting bigger.

So what changed?

The way we move money has evolved faster than most industries. Reports suggest the global money transfer app market is set to grow by over $52 billion by 2030, with steady double-digit growth. Well, this is a clear signal. Businesses are investing heavily because user behavior has already shifted. That’s why focusing on an advanced money transfer app development has become of utmost importance to the FinTech market.

But the real question is,

Are users comparing your app to a bank anymore? Or are they comparing it to the best digital experiences they use every day?

Because today, speed is expected. Transparency is expected. People want to know where their money is, how long it will take, and what it will cost, instantly. If your app cannot deliver that, someone else will.

This shift is opening doors for everyone. Startups now have a chance to enter spaces that were once dominated by legacy systems. At the same time, traditional financial institutions are under pressure to rethink their entire payment infrastructure, not just to keep up, but to stay relevant.

But building in this space is not as simple as moving fast and launching an app.

How do you handle compliance from day one?

How do you ensure transactions are secure at scale?

How do you build something that can grow without breaking?

These are the real challenges.

In the sections ahead, we will break down exactly how to approach money transfer app development in 2026, step by step, with a clear focus on technology, compliance, and building something that actually lasts.

Let’s be honest. When was the last time you paid someone in cash?

Or waited hours for a bank transfer to go through?

In India, that shift did not just happen gradually. It exploded with the introduction of the Unified Payments Interface (UPI). What started as a simple way to transfer money has now become the backbone of how India pays, sends, splits, and even lives financially.

.png)

Before UPI, sending money meant:

Now?

You scan a QR code, enter a UPI ID, or just tap a contact. Done in seconds.

That simplicity is exactly why UPI changed everything.

UPI is not just popular. It dominates.

And here’s the interesting part.

UPI is not just growing in value. It is growing in frequency. Smaller, everyday transactions are shifting to digital, which means people are using it for everything.

Tea? UPI.

Auto ride? UPI.

Rent split? UPI.

Well, the question should be,

Why did UPI succeed where many payment systems failed?

It’s because UPI solved real problems.

It removed friction completely.

Think about these situations…

This is where UPI changed the game. It brought digital payments not just to urban users, but deep into small businesses and rural markets.

In fact, the drop in average transaction size shows that UPI is now used for daily, low-value purchases, not just big transfers.

Now ask yourself:

Would you use an app that takes hours to transfer money?

Would you pay extra fees for something that should be instant?

Probably not!

UPI has completely reset user expectations.

People now expect:

Anything slower feels outdated.

Even though UPI is already massive, the growth is far from over.

By 2030, India is expected to further strengthen its position as a global leader in real-time payments, with UPI at the center of that ecosystem.

UPI did not just introduce a new payment method. It changed behavior. It made digital payments feel normal. Effortless. Instant. And now the bigger question is- If UPI has already set the standard in India, how do you create a money transfer app that can match or exceed that experience? Because today, you are not competing with banks anymore. You are competing with UPI-level simplicity.

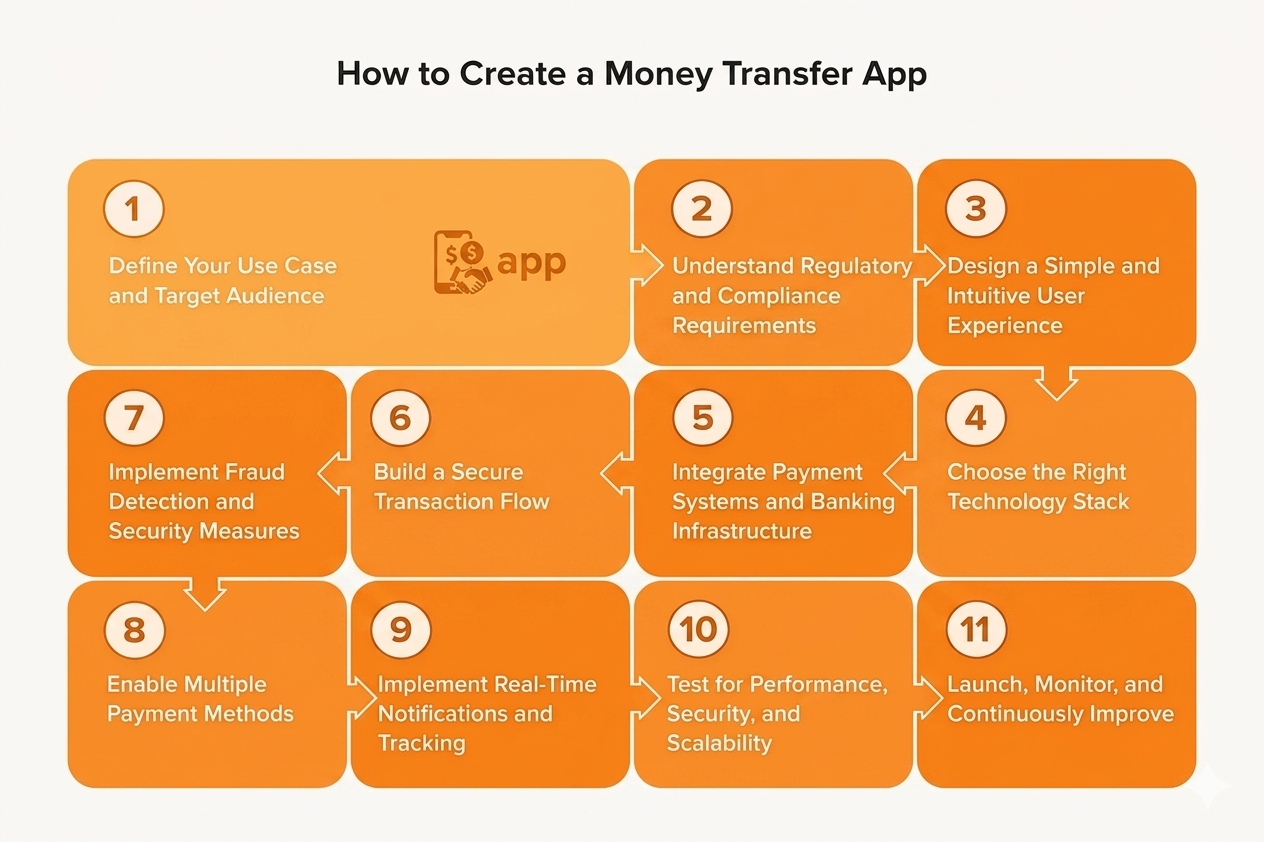

Building a money transfer app today is not just about enabling transactions. It is about creating an experience that is fast, secure, scalable, and trusted from day one. With rising user expectations and strict regulations, every step needs to be planned carefully.

Here is how you can approach building a money transfer app the right way…

Start with clarity.

Are you building:

Understanding your users helps you design features, workflows, and even compliance requirements.

Money movement is highly regulated.

You need to align with:

Getting this right early avoids major roadblocks later.

If sending money feels complicated, users will drop off.

Focus on:

The goal is to make transfers feel effortless.

Your tech foundation determines how well your app performs at scale.

This includes:

A strong tech stack ensures speed and reliability.

To actually move money, your app needs to connect with:

These integrations make real-time transfers possible.

Security is critical when dealing with financial data.

Your app should include:

Every transaction must be protected without slowing down the experience.

This is where modern apps stand out.

Embedding AI helps you:

At the same time, advanced security layers like tokenization and biometric authentication ensure safer transactions with less friction.

Give users flexibility.

Support options like:

More choices mean higher adoption and better user experience.

Users want visibility.

Your app should provide:

This builds trust and transparency.

Before launch, test everything.

Focus on:

Even small issues can impact user trust.

Going live is just the beginning.

Post-launch, you need to:

Creating a money transfer app is not just about building features. It is about building trust. At Antino, the approach focuses on combining strong technology, seamless user experience, and advanced security to create solutions that are not only functional but future-ready.

Because in today’s world, users do not just want to send money. They want it to be instant, simple, and completely reliable.

Building a money transfer app is not a fixed-cost project. It depends on how far you want to go, from a simple peer-to-peer app to a full-scale platform handling cross-border payments, compliance, and millions of transactions.

One thing is clear though. You are not just paying for development. You are investing in security, compliance, scalability, and user trust.

Before jumping into numbers, here is what really impacts your budget:

In 2026, most money transfer apps typically fall within this range:

The final cost depends on how complex your product vision is.

Costs increase when you:

Costs can be optimized when you:

Building the app is just step one. After launch, you will also spend on:

The cost of building a money transfer app is not just about development. It is about creating a system that people trust with their money. A smart approach is to start lean, validate your product, and then scale with the right features over time. Because in this space, it is not about who builds first. It is about who builds something that actually works at scale.

Not all money transfer apps are built the same. Some are designed for quick everyday payments, while others handle cross-border remittances or business transactions. The type of app you build depends on your users, use case, and scale.

Let’s break down the major types of money transfer apps, along with real-world examples you already know.

These are the most commonly used apps for everyday transactions between individuals.

What they do:

Allow users to send and receive money instantly using phone numbers, UPI IDs, or linked bank accounts.

Key features:

Examples:

Where they are used:

Splitting bills, paying rent, sending money to friends or family.

These apps focus on transferring money within a country, often integrated deeply with local banking systems.

What they do:

Enable users to transfer funds between banks quickly and securely.

Key features:

Examples:

Where they are used:

Utility payments, business payments, local transactions.

These apps are designed for cross-border money transfers.

What they do:

Allow users to send money across countries with currency conversion.

Key features:

Examples:

Where they are used:

Sending money to family abroad, freelancer payments, international business transactions.

These apps store money digitally and allow users to transact without directly using a bank account every time.

What they do:

Let users load money into a wallet and use it for payments or transfers.

Key features:

Examples:

Where they are used:

Online shopping, subscriptions, small daily payments.

.png)

These apps are built for businesses to manage payments at scale.

What they do:

Handle bulk payments, vendor payouts, payroll, and invoicing.

Key features:

Examples:

Where they are used:

Enterprise payments, vendor management, subscription billing.

These apps use blockchain technology for transferring money.

What they do:

Enable users to send digital currencies globally without traditional banks.

Key features:

Examples:

Where they are used:

Crypto trading, global transfers, digital asset management.

These apps go beyond just money transfers and offer a complete financial ecosystem.

What they do:

Combine banking, payments, savings, and investments in one app.

Key features:

Examples:

Where they are used:

Managing overall finances along with payments.

The type of money transfer app you choose to build depends on your business goals and target audience. Are you solving for quick everyday payments? Or building a global financial platform?

Because today, users do not just want to send money. They want speed, transparency, flexibility, and a seamless experience across every transaction.

A money transfer app today is expected to do much more than just move money. Users want speed, transparency, security, and a smooth experience every single time. If even one of these feels off, they switch apps instantly.

So what does it actually take to build a money transfer app that users trust and keep coming back to?

Here are the must-have features you should not miss…

First impressions matter.

Users should be able to:

If onboarding feels long or complicated, most users drop off before even making their first transaction.

Since financial data is involved, security needs to be strong but not annoying.

Include:

This ensures safety while keeping access quick.

This is the core of your app.

Users should be able to:

The goal is simple: make sending money feel effortless.

Nobody wants to wait for money to arrive.

Your app should support:

Speed builds trust.

Different users prefer different payment methods.

Your app should support:

More options = better adoption.

Users want visibility.

Include:

This helps users stay informed and in control.

Communication is key.

Notify users about:

This keeps everything transparent.

.png)

Security should be layered across the app.

Key features include:

Users need to feel that their money is safe at all times.

This is where modern apps stand out.

AI can help:

It works silently in the background but adds huge value.

If your app supports international transfers, this is essential.

Include:

This improves user confidence in cross-border payments.

Users need quick help when something goes wrong.

Provide:

Fast support improves user retention.

It is not always about sending money.

Users should also be able to:

This makes the app more useful in daily scenarios.

Make payments more intuitive.

Allow users to:

This reduces friction.

For the business side, this is critical.

Include:

This helps you manage and scale operations efficiently.

Your app should grow with your users.

Ensure:

Because even a small delay can impact trust.

A great money transfer app is not built by adding features randomly. It is built by understanding what users actually need and delivering it in the simplest way possible. At the end of the day, users do not care about how complex your backend is. They care about one thing. Can they send money instantly, safely, and without any hassle?

Enterprises do not just need an app, they need a system that can handle scale, security, and compliance without slowing down growth. That is exactly where Antino steps in. We as a leading Fintech app development company helps building real-time transaction systems to integrating banking infrastructure and advanced security layers, the focus is always on creating solutions that are reliable and future-ready.

Whether it is handling high transaction volumes, embedding AI for fraud detection, or ensuring compliance across regions, Antino helps enterprises move faster without compromising on trust.

If you are planning to build a money transfer app that users actually rely on, Antino brings the right mix of strategy, technology, and execution. The goal is to create a seamless, secure, and scalable experience that grows with your business. Want to turn your idea into a high-performing payment platform? Let’s connect and make it happen!

.png)