Have you ever paused to think about how fast money moves today? No paperwork, no waiting in line, just a few taps, and it’s done. For industry leaders, this raises a crucial question: Are we doing enough to keep pace with the evolving consumer expectations in the P2P payments space?

Global’s peer-to-peer (P2P) payments landscape has seen an extraordinary transformation over the last few years. What once relied heavily on cash or time-consuming banking processes is now dominated by instant, smartphone-driven transactions through P2P apps. But what really sparked this shift?

The surge in P2P payment app adoption is the result of multiple converging factors:

Also, the global P2P payment market size is anticipated to reach around USD 16.21 trillion by 2034, growing at a CAGR of 18.10% from 2025 to 2034.

Fintech platforms like Venmo, Zelle, Revolut, Paytm, M-Pesa, and many others are at the forefront of this transformation, offering instant, secure, and user-friendly money transfer capabilities. This surge is a wake-up call for fintech players. As P2P payments continue to evolve, businesses must ask themselves:

Are we building P2P app platforms that match the expectations of a digitally empowered world?

Are we investing in security, scale, and user experience to stay relevant in this hyper-growth market?

But as usage scales, so do expectations.

For global fintech leaders, the question isn’t whether to innovate in this space; it’s how fast you can scale while keeping your platform secure, compliant, and frictionless across markets. Are your systems future-ready? Can your architecture support real-time volumes without trade-offs in user experience?

In the sections ahead, we’ll explore the key drivers behind this explosive growth and what fintech innovators must do to stay relevant in a rapidly evolving financial landscape.

But let’s just understand P2P payments first

Peer-to-peer (P2P) payment systems have transformed the way people exchange money, making transactions faster, easier, and more accessible.

Peer-to-peer (P2P) payments refer to the direct exchange of money between individuals through digital platforms or mobile apps. These systems allow users to send or receive funds without involving traditional banks or physical cash. By leveraging technology, P2P payments offer a simple and efficient alternative to conventional payment methods by enabling quick transfers anytime, anywhere.

With P2P transactions becoming the new standard for everyday money transfers, building a peer-to-peer payment app has become a strategic opportunity. But creating a secure, scalable, and user-friendly P2P app involves more than just writing code. It demands a deep understanding of technology, user behavior, compliance regulations, and financial infrastructure.

Here’s a step-by-step breakdown to help you get started…

Before diving into development, it’s critical to define:

Clear answers here will shape your entire product journey.

Your app needs to be fast, secure, and scalable. Here’s what to consider:

Handling financial data comes with responsibility. You must ensure:

Your app should be built with privacy by design because security cannot be an afterthought.

Start with a Minimum Viable Product (MVP) that includes:

Later, you can scale up with features like bill-splitting, recurring payments, QR payments, voice-assisted transfers, or even crypto wallet support.

Unless you're licensed to operate as a financial institution, you’ll need to integrate with third-party services or partner banks. Choose providers that offer:

Once built, the app should go through multiple rounds of testing:

Gather feedback, iterate on UI/UX, and prepare to scale.

A soft launch (beta release) can help you understand how real users interact with your app. Once the product is stable, plan a full-scale release with:

Developing a P2P payment app is about building trust, enabling convenience, and meeting the financial needs of today’s digital-first users. The goal is to create an app that’s not only secure and fast but also simple enough for anyone to use, from a college student in California to a vendor in Delhi. If you're ready to step into the fast-evolving world of digital payments, partnering with the right FinTech app development team can make all the difference.

In today’s hyper-personalized, fast-moving fintech space, simply offering money transfers isn’t enough. To stand out, P2P payment apps must evolve from being transaction tools to becoming intelligent financial companions. That’s where AI-driven features step in by adding speed, security, personalization, and smarter decision-making.

Here are some of the newest AI-powered features you should consider when building a modern, competitive P2P payment app…

With millions of microtransactions happening every second, fraudsters are constantly looking for loopholes. AI can help stay ahead of them by:

AI-powered fraud detection not only strengthens security but also minimizes false positives, ensuring seamless transactions for genuine users.

AI in banking can analyze a user’s transaction history, behavior patterns, and contacts to provide intelligent nudges like:

This creates a more proactive and context-aware payment experience that saves users time and increases app engagement.

Today’s users expect instant help, without waiting on hold or navigating long FAQs. AI-driven chatbots can:

Modern NLP (Natural Language Processing) tools like OpenAI's GPT models or Google Dialog Flow make these bots feel almost human.

A great P2P app can double up as a lightweight financial advisor using AI:

This feature not only increases app stickiness but positions your product as a value-added financial tool.

With AI voice recognition technology becoming increasingly accurate, voice-based commands are making their way into finance. Features like:

...can all be handled hands-free using AI-powered voice assistants, enhancing accessibility and convenience for users on the go.

While still emerging, emotion AI is beginning to make its mark. Some fintechs are exploring AI models that interpret tone or facial expressions (via camera or mic permissions) to adjust user interfaces accordingly. For example:

This kind of responsive design creates more empathetic and user-centered experiences.

AI can automatically tag and classify transactions (e.g., utilities, groceries, rent, entertainment), helping users:

This reduces manual effort and builds long-term trust in the platform.

AI can observe how individual users navigate your app and dynamically adjust:

This makes the experience feel more intuitive and personalized without any manual input from the user.

AI has literally become the secret ingredient behind the smartest, most seamless P2P payment platforms today. From fraud prevention to user engagement, the right AI-led features can drive adoption, retention, and competitive edge.

If you’re building a next-gen P2P app, integrating these intelligent features early in your roadmap could be the key to long-term success in a crowded market. But before starting the development process, you should be aware of all the compliances too. Let’s take a look…

When it comes to building a peer-to-peer (P2P) payment app, innovation and user experience often take center stage. But beneath every sleek interface and seamless transaction lies the backbone of your platform: compliance. In the highly regulated world of digital finance, ensuring your app meets legal and regulatory standards is non-negotiable.

Whether you're operating locally or scaling globally, compliance is what keeps your P2P app trustworthy, secure, and legally viable.

P2P apps handle sensitive user data, financial transactions, and identity verification by making them high-risk targets for fraud, data breaches, and financial crimes like money laundering or terror financing. Governments and financial regulators enforce strict rules to protect users and the financial ecosystem. Failing to comply can result in:

In short, compliance is an ongoing foundation of your product lifecycle.

KYC regulations require P2P platforms to verify the identity of users before they can access financial services. Depending on the region, KYC may involve:

KYC ensures that your platform is used by legitimate users and helps reduce fraud and identity theft.

AML laws are designed to detect and report suspicious financial behavior, preventing money laundering and financial terrorism. For P2P apps, AML compliance may include:

If your app handles debit/credit card transactions, you're required to comply with Payment Card Industry Data Security Standards (PCI DSS). This ensures cardholder data is stored, processed, and transmitted securely.

Compliance involves:

User data protection laws vary by region but are critical to every fintech product development process. Your app must comply with:

Make sure your platform has a clear privacy policy, data encryption practices, and consent-based data collection.

Depending on your geography, you may need licenses or registrations from local authorities:

Each license has its own set of capital requirements, audit obligations, and reporting standards.

Most jurisdictions define daily/monthly transaction limits, especially for unverified users. These limits are put in place to prevent misuse and help flag unusual activity.

You must also ensure:

Building a compliant P2P app is about building user trust, investor confidence, and long-term sustainability. The most successful digital payment platforms today aren’t just the most innovative, they’re the most compliant.

So, if you're developing a P2P payment solution, treat compliance not as a hurdle, but as a core pillar of product design because, in fintech, trust is earned, not assumed. But how can you make your P2P app more engaging for your users?

In the competitive world of digital payments, functionality alone isn’t enough to keep users coming back. Today’s users, especially Gen Z and millennials, expect an experience. That’s where gamification steps in.

Gamification refers to the integration of game-like elements such as points, rewards, leaderboards, challenges, or badges into non-gaming environments to enhance user engagement and motivation. When applied to fintech and payment transfer apps, it transforms routine financial interactions into engaging, habit-forming experiences.

Sending or receiving money isn’t inherently exciting. But gamification can:

By adding layers of interactivity and rewards, gamification reshapes user behavior while building brand loyalty.

Users earn points for completing specific actions such as:

These points can then be redeemed for cashback, gift cards, or in-app perks.

Example: Google Pay India offers “scratch cards” after transactions, with rewards or cashback.

Creating a sense of accomplishment through badges can encourage deeper interaction. For example:

Users love to track progress and feel a sense of recognition.

Encourage users to take specific actions within a set time frame:

These time-based challenges promote frequency and app stickiness.

.png)

Introduce a competitive element by letting users see how they rank against friends or within a user community:

Social bragging rights combined with rewards can drive powerful engagement loops.

Gamified interfaces like spinning a wheel after every transaction or unlocking a mystery box keep users curious and entertained.

These features tap into behavioral psychology, especially the variable reward system that drives dopamine-fueled user engagement.

Help users set savings or spending goals and reward progress:

Over time, users can unlock new levels of "financial fitness" or even personalized money tips.

Emotional Connection with Brand: Fun and rewarding experiences foster deeper brand loyalty.

Gamification is about making everyday financial actions more engaging, intuitive, and rewarding. When done right, it turns passive users into active participants and builds a stickier product experience.

As the fintech space becomes increasingly crowded, gamification could be the edge that sets your platform apart.

Gamification is about making everyday financial actions more engaging, intuitive, and rewarding. When done right, it turns passive users into active participants and builds a stickier product experience.

As the fintech space becomes increasingly crowded, gamification could be the edge that sets your platform apart.

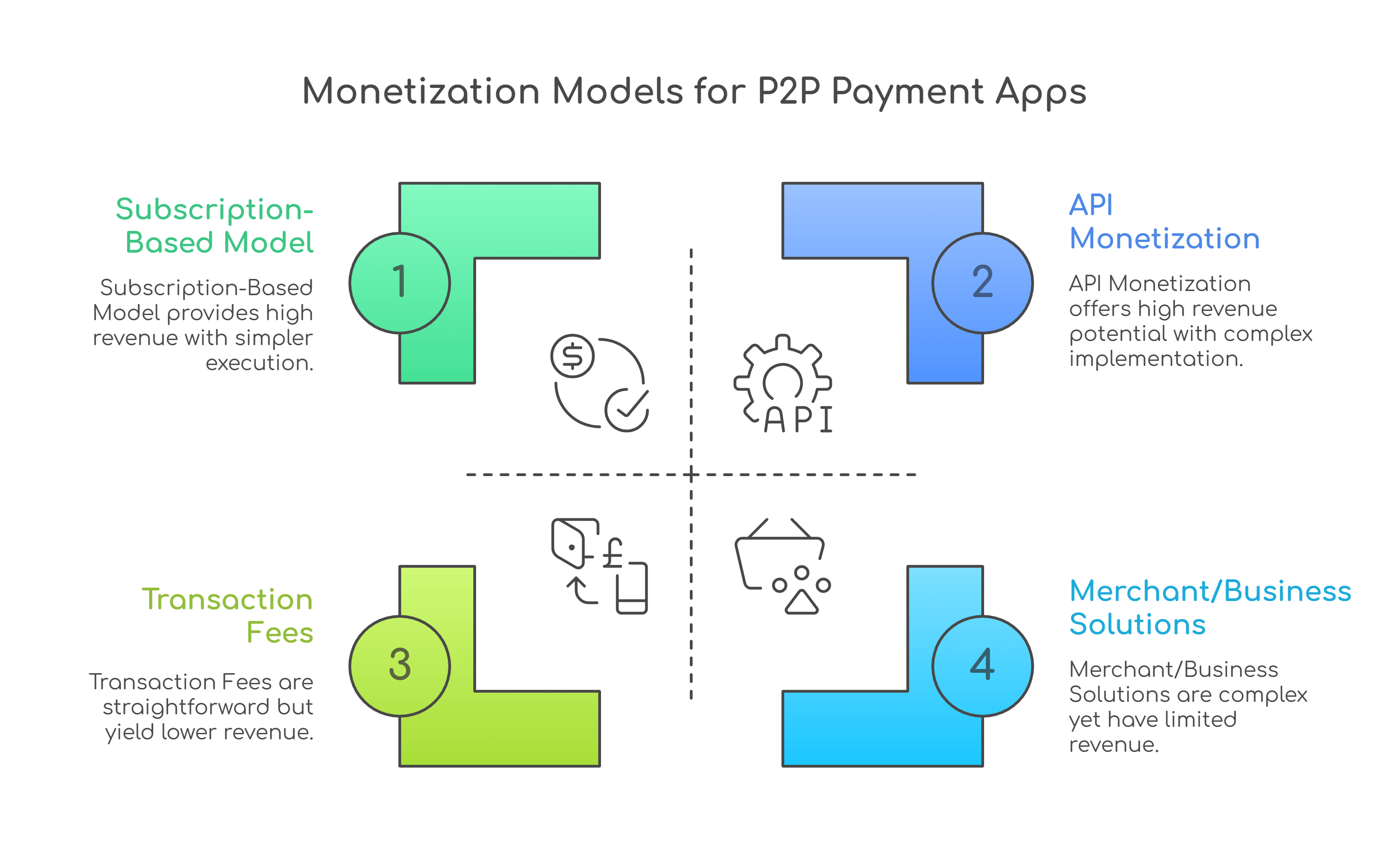

While seamless transactions and engaging UX are essential for user adoption, the long-term success of any payments app depends on one key factor: a sustainable monetization strategy. With rising competition in the fintech space, building a free-to-use platform may attract users initially, but without a clear revenue model, scaling becomes difficult.

Whether you're building a peer-to-peer (P2P) app, digital wallet, or a broader payment ecosystem, choosing the right monetization model or a combination of them is critical for profitability and long-term growth.

One of the most straightforward models. The platform charges a small fee on every successful transaction. These could be:

This model works best when the value delivered is high enough to justify the fee.

Offer basic services for free while charging for advanced features. This model is popular in SaaS-style fintech platforms where users may pay for:

Example: Users can send up to $1,000/month for free, but need a premium plan to increase their limits or remove ads.

If your payment app issues physical or virtual debit cards (in partnership with banks or card networks), you can earn a portion of the interchange fee every time users swipe their cards. Interchange fees are paid by the merchant’s bank to the card-issuing institution.

This model has been a major revenue stream for platforms like Cash App and Venmo through their branded debit cards.

If your app supports payments for small businesses, freelancers, or creators, you can monetize by offering value-added services such as:

Monetization comes from charging a small percentage per transaction or offering a monthly business toolkit subscription.

You can partner with financial institutions, lending services, insurance companies, or wealth management platforms to promote relevant offers inside your app. Whenever a user signs up through your referral link, you earn a commission.

Example: Promote a credit card or personal loan offer inside the app and earn a fee per qualified user.

When users keep money in their wallets, your platform can deposit that idle balance in interest-bearing accounts. The interest earned (called float income) becomes a revenue stream.

This model is subject to regulatory restrictions and often requires licenses or partnerships with banks or financial custodians.

Though not always preferred due to user experience concerns, ads and sponsored listings can be a source of revenue. Options include:

This works better in markets where ad tolerance is high and user volume is significant.

Payment apps can serve as a distribution channel for various financial products, such as:

Revenue is generated through lead generation, partnerships, or interest spreads.

Offer users access to exclusive features, enhanced limits, or value-added services through monthly or yearly subscriptions. Features may include:

This model ensures recurring revenue and works well when value delivery is consistent.

If your app evolves into a platform offering payment APIs or SDKs to other apps, you can monetize based on:

This works best for fintech infrastructure providers or payment aggregators.

The most successful platforms often use a hybrid approach for balancing user experience with sustainable revenue streams. The key is to understand your audience, deliver continuous value, and monetize in ways that feel natural rather than intrusive.

Whether you’re targeting consumers, businesses, or developers, designing your monetization strategy early on will help build a scalable and profitable product. But what’s the cost of developing a P2P payments app?

Building a P2P money transfer app can be a game-changing move in today’s digital economy, but like any fintech product, it comes with a wide range of costs depending on the app’s complexity, features, platform, and development approach.

Whether you're planning to build a basic MVP, a fully-featured mid-level app, or a high-end enterprise-grade platform, the total development cost will vary significantly based on:

Here’s a breakdown of what goes into the development cost:

The cost of developing a P2P money transfer app depends entirely on your vision, scale, and required feature set. For startups, starting with an MVP and gradually scaling features can be a smart way to enter the market without breaking the bank. For enterprises, investing in scalability, AI-powered fraud detection, and robust infrastructure ensures long-term growth and user trust.

So, if you're exploring P2P app development, choosing the right tech partner with expertise in secure financial systems can drastically reduce both risk and cost.

The peer-to-peer (P2P) payments market has witnessed a consistent and steep upward trajectory in recent years. From casual bill-splitting among friends to cross-border remittances, P2P payments have evolved into a mainstream financial tool. But what’s fueling this impressive and sustained growth?

Let’s break down the key reasons behind the sharp incline in the P2P market’s growth graph…

The global rise in smartphone adoption and affordable mobile internet has dramatically expanded the reach of digital financial services. Millions of people, especially in emerging economies, are accessing banking services for the first time through mobile apps.

Cashless transactions are no longer a niche behavior, they’re the norm. Today’s users demand speed, simplicity, and convenience, which traditional banks often fail to provide in real-time.

Many governments and regulatory bodies across the globe are actively encouraging digital payment adoption to foster financial inclusion and transparency. Initiatives include:

These efforts reduce reliance on cash, enhance traceability, and drive mass-scale adoption of P2P solutions.

Earlier, users were skeptical of digital wallets and online transfers. But today, leading fintech apps invest heavily in security, compliance, and user education, which has resulted in increased trust.

P2P apps are no longer limited to just sending money to friends. They now support:

This diversification of use cases is increasing daily touchpoints and encouraging higher transaction volumes.

Unlike legacy banking systems, modern P2P apps are built on cloud-native, API-first architecture, making them:

This enables even small startups to build and scale globally with limited overhead, fueling market expansion.

When companies like Apple (Apple Pay), Google (GPay), Meta (Novi), and PayPal (Venmo) entered the space, the P2P ecosystem gained massive visibility and credibility.

These platforms come with:

Their presence has normalized digital payments and pushed even reluctant users into the P2P ecosystem.

As economies become more interconnected, there’s a rising need for real-time international transfers. P2P apps are stepping up to provide:

This trend is particularly strong among migrant populations and freelancers working across borders.

Many P2P apps are adding gamified experiences, rewards, challenges, referrals, to increase engagement. These features:

This smart blending of finance and fun contributes directly to rising transaction volumes and user retention.

AI is powering personalized financial insights, smart notifications, fraud detection, and intelligent automation in P2P apps. The smarter the app becomes, the more users rely on it for daily financial needs, driving long-term growth.

The upward-sloping graph of the P2P payments market reflects a global shift in how people think about and manage money. It’s driven by innovation, infrastructure, policy, and people’s need for instant, intuitive financial solutions.

As the world continues to move toward digital-first economies, the P2P payments sector is poised to become not just a support tool but a central pillar in the financial lives of millions.

At Antino, we build reliable, future-ready platforms engineered for speed, security, and scale. With deep domain expertise in fintech and digital finance, our teams understand what it takes to craft a seamless peer-to-peer experience. From user-friendly onboarding and real-time transfers to AI-powered fraud detection, we ensure every layer of your app is secure, scalable, and compliant with global financial standards.

Whether you’re targeting a niche audience or building for mass adoption, we tailor our Fintech app solutions to your business goals, leveraging the latest tech stacks, robust APIs, and cloud-native infrastructure. Let’s build something that not only meets today’s expectations but also sets you up for tomorrow’s growth. Reach out to Antino, and let’s turn your P2P payment idea into a powerful product.

.png)